![Metalswap Knowledge [BLOG]-Apr-23-2024-04-10-28-2103-PM](https://blog.metalswap.finance/hs-fs/hubfs/Metalswap%20Knowledge%20%5BBLOG%5D-Apr-23-2024-04-10-28-2103-PM.png?width=1800&height=900&name=Metalswap%20Knowledge%20%5BBLOG%5D-Apr-23-2024-04-10-28-2103-PM.png)

Currently in DeFi the most widely used and highest volume derivative instrument is undoubtedly the perpetual swap.

This is particularly favoured by traders as it has relatively low fees, no expiration date and because it offers the possibility of using very high leverage.

However, the perpetual swap has a significant problem: a variable fee that can sometimes reach up to 75% per year, known as the funding rate.

The funding rate is the main mechanism behind the pricing of a perpetual swap.

On a perpetual DEX, there are indeed two prices for each pair: the market price, which is the official external price and the specific price for that pair on that particular perpetual DEX.

These two prices should theoretically always be equal, but in reality, they can diverge if there is a majority of positions on one side, long or short.

The funding rate is a fee paid by the majority positions to the minority positions, ensuring there is always an incentive to open trades that bring the perpetual swap price closer to the market price.

How much does the funding rate cost?

When trading on a DEX or a CEX of perpetual swaps, often only the fees at the time of opening a position are considered, without taking into account what might be the most important fee, namely the funding rate.

But how much does it impact?

Let's first consider some factors. As the crypto market is generally a positive and bullish market, long positions are typically more prevalent than short positions.

This means that, in most cases, the price of the perpetual swap tends to be higher than the real market price.

This means that in most scenarios, it is the long positions that pay the funding rate, while the short positions receive it.

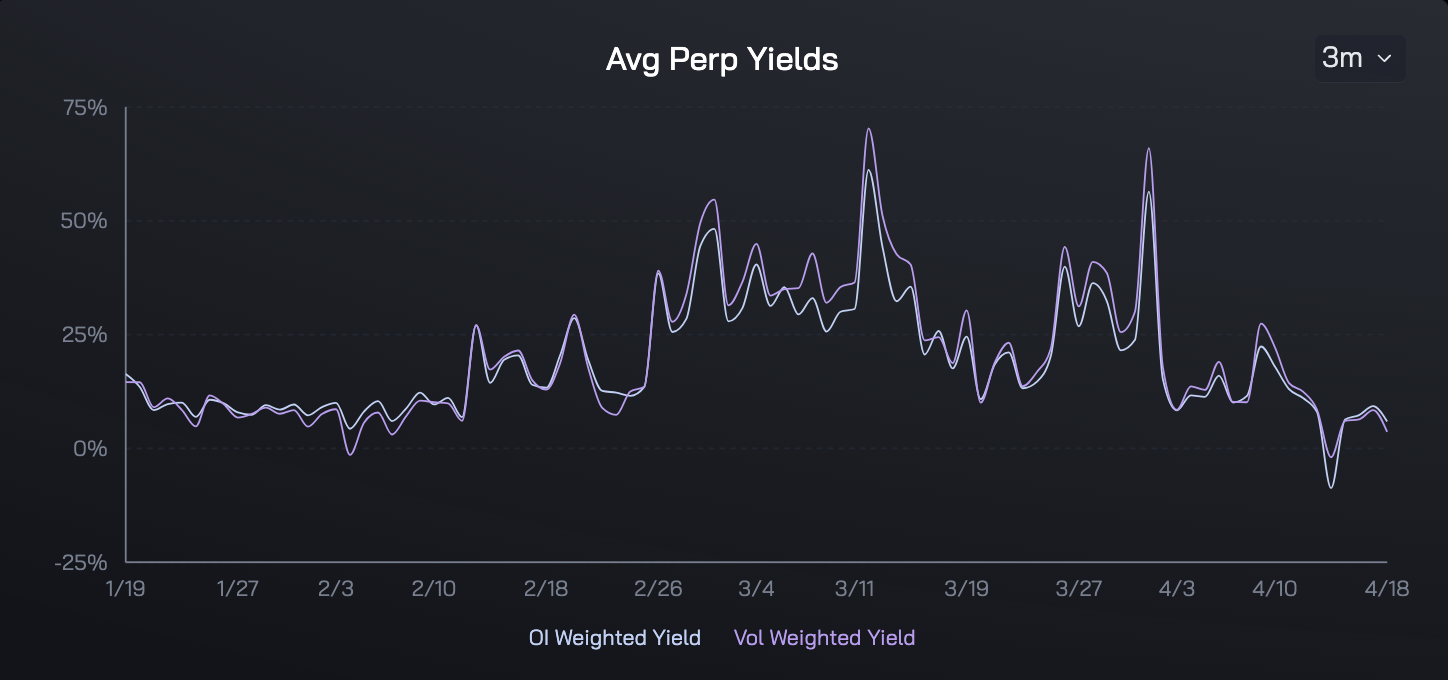

Let's analyze what the average funding rate cost has been over the last three months among the major DEXs and CEXs of perpetual swaps on the ETH/USD pair.

Source: Ethena dashboard

As we can see, there are peaks that approach a 75% of funding fee for the long positions, obviously corresponding to particularly positive market moments where traders have opened almost exclusively long positions.

This means that everyone who has opened speculative long positions on ETH has had to pay this fee, while those who have opened short positions have earned it.

If instead of opening it on a perpetual exchange, the trader had opened a long position on MetalSwap, they would not have paid any funding rate.

Trading on MetalSwap without the funding rate

We understood that it is typically the long positions that have to pay this fee, but obviously, in bear market periods where most positions are short, the situation could reverse.

We have also understood that the funding rate tax is unpredictable and can reach very high levels, especially during times when the market has significant and decisive price movements.

This unpredictable variable could break the strategy of a trader who opens a long position for extended periods of time.

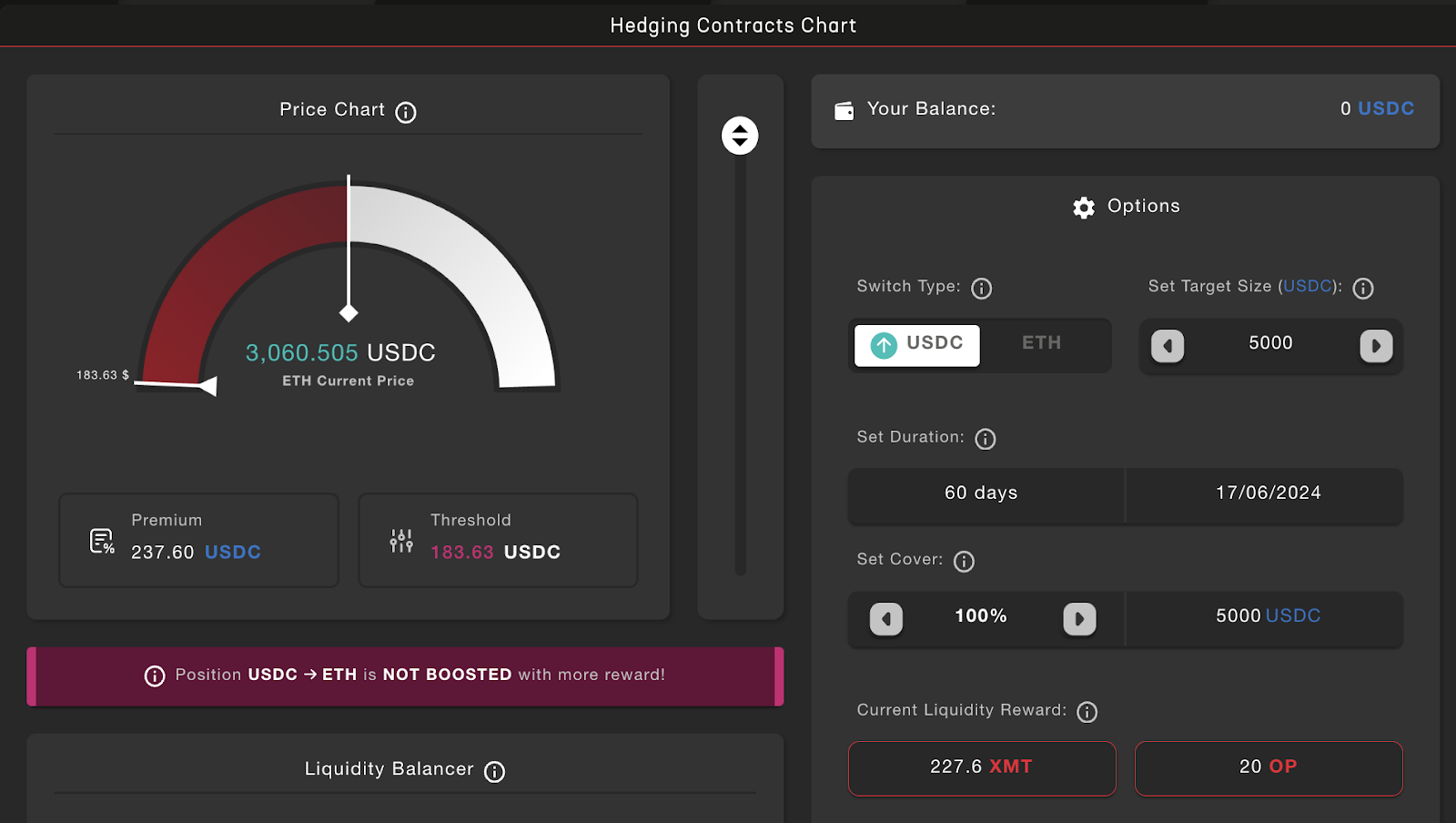

Now let's see how to open a long position on MetalSwap, without paying a funding rate.

The first step is obviously to reach the official dApp.

Then select the blockchain you want to operate on, choosing from Ethereum, Optimism and Linea. Then, finally select the asset from those available.

In this case, we will show a long position on the Optimism chain on the ETH asset.

Obviously, the funding rate becomes relevant on positions opened over a long period and in this case, we will give an example of a position opened for 60 days.

The target size set is $5000 and the premium required by the MetalSwap dApp is $237, corresponding to 4.74% of the total position.

Also considering the 20 OP tokens as liquidity rewards, the fee further decreases by $45, coming to $192, corresponding to 3.84%.

The same position opened on a perpetual DEX, besides the fixed fees of opening and closing that can vary from 0.05% to 0.20%, also incurs the cost of the funding rate, which, as we have seen, is unpredictable and can even reach peaks of 75% annualized.

MetalSwap proves to be a more economical tool in phases where the market shows decisive and sharp price movements upwards.

Similarly, if there is a situation with most positions being short, MetalSwap will be cheaper than a short on a perpetual.

Why doesn't MetalSwap have a funding rate?

MetalSwap eliminates the need for a funding rate by utilizing hedging contracts. These contracts form the basis of the derivative instrument known as hedging swaps.

To understand more about how these instruments work and their benefits, you can refer to the detailed explanation provided in a dedicated article.

Conclusions

In the last bull market of 2021, in the first 3 months of that year, the average funding rate was +47% and if another similar bull market starts in the coming months, a similar funding rate situation will occur.

In this case, operating with long positions on perpetual will again be extremely expensive and solutions like MetalSwap that do not use the funding rate position themselves as a necessary alternative in the market.

Try MetalSwap today and participate in the Swap Competition that is currently running!

Over 1000 USDC as prizes and 3300 OP tokens to be distributed as liquidity rewards!

-The DeFi Foundation

✎ What is MetalSwap?

MetalSwap is a decentralized platform that brings Hedging Contracts on financial markets with the aim of providing coverage to those who work with Digital Assets and an investment opportunity for those who contribute to increase the shared liquidity of the project. Allowing the protection for an increasing number of operators.

With MetalSwap we enable Hedging Contracts on the DeFi field, AMM style.