![MetalSwap Insight - Vol.7 [BLOG]](https://blog.metalswap.finance/hs-fs/hubfs/MetalSwap%20Insight%20-%20Vol.7%20%5BBLOG%5D.png?width=1800&height=900&name=MetalSwap%20Insight%20-%20Vol.7%20%5BBLOG%5D.png)

There is no doubt that in the last year one of the sectors that has grown the most within DeFi, both in terms of traded volumes and total value locked, is that of financial derivatives. Mirroring traditional markets, where derivative instruments dominate in terms of volumes, a similar trend is now evident in decentralized finance, with trades completed within derivative instruments far surpassing spot trades.

In today's article, we propose an analysis of this DeFi sector, with a particular focus on volumes, fees, total value locked and all the main parameters that can tell us the state of this flourishing market.

Perpetuals dominate the scene

There is undoubtedly one derivative instrument that has won the throne within the derivatives market and that is the perpetual. Similar to futures, the perpetual instrument allows investors and traders to expose themselves to the price of various assets, using margin and also applying financial leverage.

However, unlike traditional finance futures, perpetuals in the crypto world differ in that they have no expiry date, but are instead managed by mechanisms such as the funding rate that allow them to maintain a value always close to that of the underlying asset they replicate.

Volumes of Perpetuals in DeFi

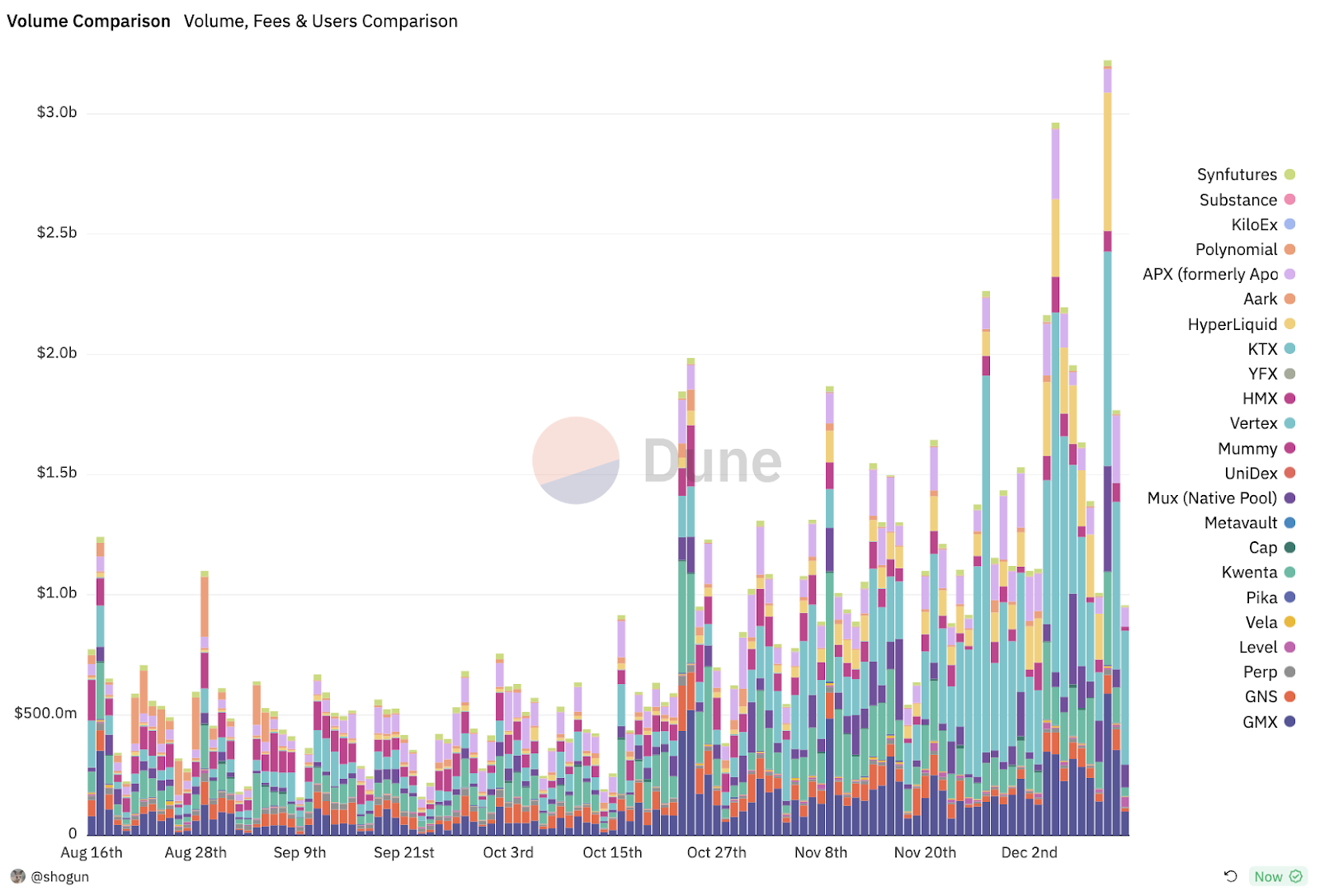

To fully analyze the volumes collected by all the major dApps offering the perpetual derivative instrument, we will examine this dashboard from Dune.

From this image, we see that, with the recent general appreciation seen in the crypto world in recent months, trading volumes within all perpetual dexes have increased, with an average in recent months hovering just below 2 billion daily trades.

In this market phase, the leading dexes are Vertex, GMX, APX and Kwenta, which together move about 80% of the entire market. Vertex recently overtook GMX, which until a few months ago was the undisputed king in terms of trading volumes. These two dexes highlight the two main philosophies of perpetual dexes currently available in the market, namely GMX-style DEXs that use an AMM for market creation, or solutions like the off-chain order book, pioneered by dApps like Vertex.

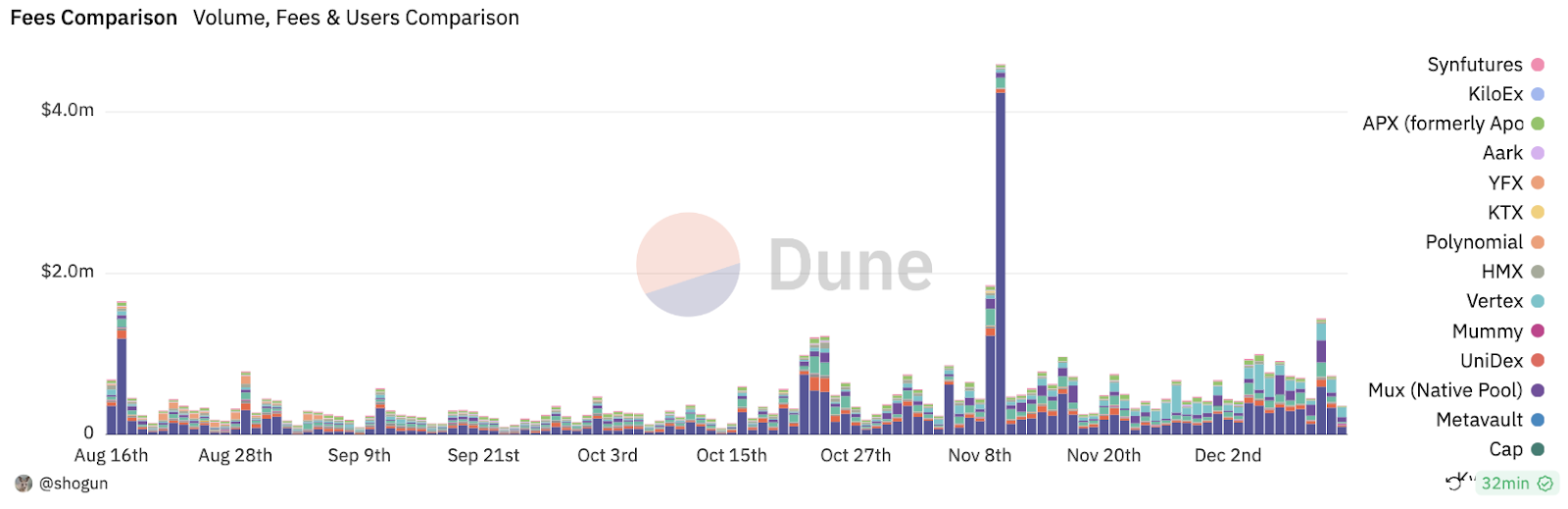

Fees Collected by Perps in DeFi

The higher the volumes, the higher the fees and thus the revenue collected by the various dApps, so it is not surprising to find the same names mentioned earlier at the top of the fee collection ranking as well.

Typically, GMX is the dApp collecting the highest commissions, followed by Vertex and MUX. Although Vertex had higher volumes in the recent period compared to GMX, the latter manages to maintain leadership in the revenue field, as it typically charges higher commissions to traders.

In general, in this market phase, the perp sector has an average collected commission of around 1 million dollars earned each day, with sessions that can reach up to 4 million like the one that occurred on November 9th.

Perps in DEX vs CEX

Perpetuals are also extremely popular in the centralized world, where they collect most of their volumes. As we can see from the graphic above, the volumes moved by centralized entities like Binance and OKX are significantly higher than those of DeFi, with a market share ratio estimated at just around 2% for decentralized finance.

The reasons for this advantage of CEXs over DEXs are certainly due to the fact that DeFi has required technological development that has allowed the creation of competitive solutions compared to the centralized versions possible only in recent months. According to some estimates and prevision, it is possible that the market share of dexes may increase in relation to CEXs, and perhaps in the future even surpass them.

Options in DeFi

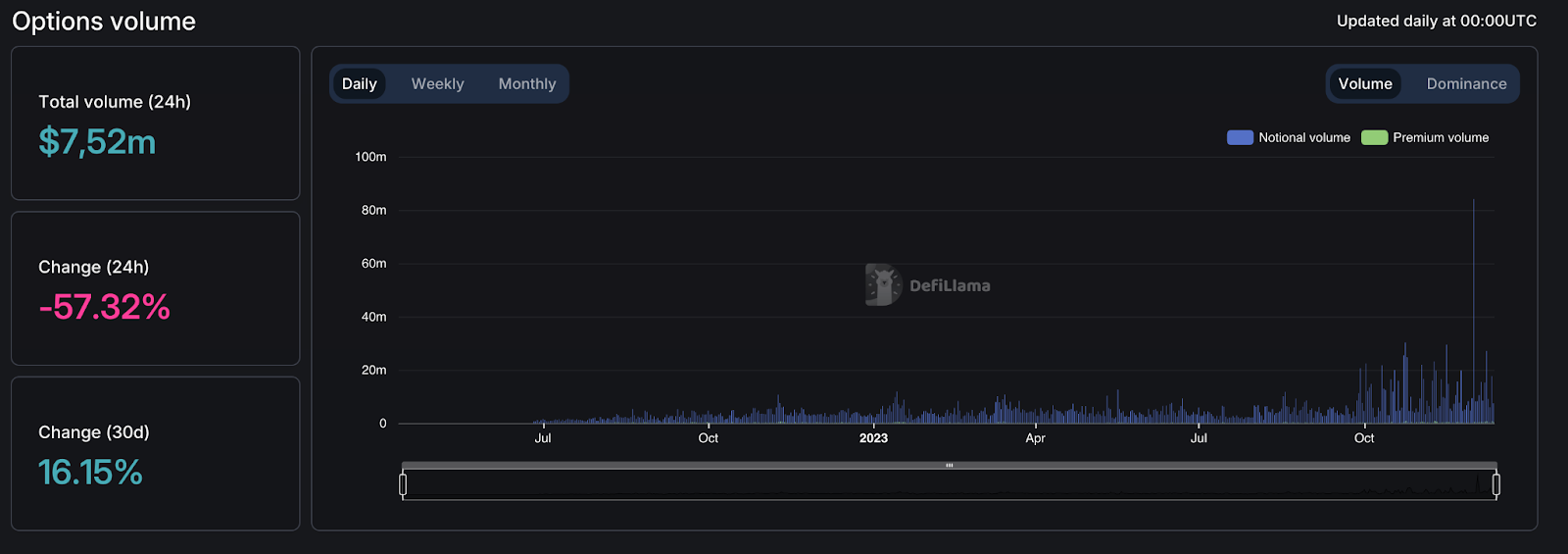

However, the options market continues to experience significantly lower trading volumes compared to perpetuals. On average, a volume of about 20 million dollars is traded daily among all the dApps that deal with options, which shows how traders within decentralized finance, to date, prefer to use much more speculative solutions like perpetuals, where leverage and commissions facilitate this type of operation.

The leading dApps at the moment in this area are Aevo, Lyra and Hegic, with Arbitrum appearing to be the blockchain of choice for this type of dApps.

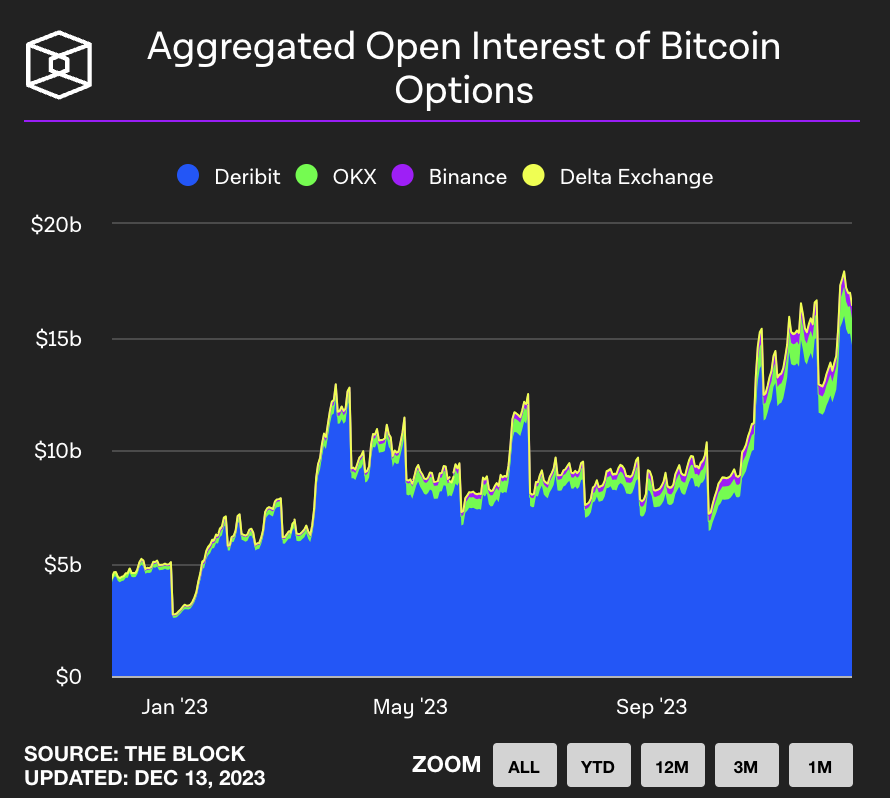

Options and CEX

Similarly to the situation in perpetuals, here too we find larger volumes in the centralized version of the instrument. Deribit is absolutely the leading exchange in the sector and alone handles about 95% of the total volumes of this sector. Other notable centralized solutions are those offered by Binance and OKX, with a total daily volume ranging from 10 to 15 billion dollars in volume.

As we have seen in this article, the perpetual instrument is undoubtedly dominating the scene, but despite this, there is still an imbalance in favour of centralized solutions that collect 98% of the total volumes of this market. Advancements in DeFi technology may lead to a gradual user shift towards decentralized solutions, also thanks to all the advantages that decentralization brings compared to the centralized wolrd.

The Hedging Contracts that MetalSwap introduced into DeFi for the first time ever had a relatively small market in the CEX ecosystem and will be the subject of a next article to complete an analysis of this specific derivative instrument.

We can therefore declare the end of this first part of analysis of derivatives markets and refer to the next article to be released soon.

-The DeFi Foundation

✎ What is MetalSwap?

MetalSwap is a decentralized platform that allows Hedging Contract on financial markets with the aim of providing coverage to those who work with Digital Asset and an investment opportunity for those who contribute to increase the shared liquidity of the project. Allowing the protection for an increasing number of operators.

With Hedging Contract we enable hedge swap transactions through the use of Smart Contracts, AMM style.

It's great to Hedge the Risk of Price volatility with MetalSwap dApp !