![Metalswap Knowledge [BLOG]-1](https://blog.metalswap.finance/hs-fs/hubfs/Metalswap%20Knowledge%20%5BBLOG%5D-1.png?width=1800&height=900&name=Metalswap%20Knowledge%20%5BBLOG%5D-1.png) Today we continue our series of articles dedicated to the Real World Assets by analyzing the most important dApps in this DeFi sector.

Today we continue our series of articles dedicated to the Real World Assets by analyzing the most important dApps in this DeFi sector.

In the first episode of this series, we provided an introduction to this world, explaining what RWAs are and which assets are most affected by this revolution.

Today's episode will be divided into the following paragraphs:

- RWA fast introduction

- Most important dApps

- The future of this sector

- Conclusions

So, without further ado, let's start this important episode.

RWA fast introduction

Real world assets, just as the name suggests, are general assets that are brought on-chain through a process of tokenization.

In theory, any real-world asset could be brought into a blockchain, although there are some assets that are preferred by tokenization dApps, including commodities, currencies, and bonds, especially American ones.

The tokenization process is certainly the most complicated step and can be primarily carried out in two ways, either through a system backed by the same asset owned in the real world, for example, Tether or Circle's stablecoins, or a synthetic tokenization system, like the assets issued by Synthetix.

The Most Important dApps

The RWA sector has seen an explosion in terms of total capitalization during the last bear market, especially thanks to the tokenization of American bonds, which managed, in that period of low interest in the sector, to bring interesting yields within DeFi.

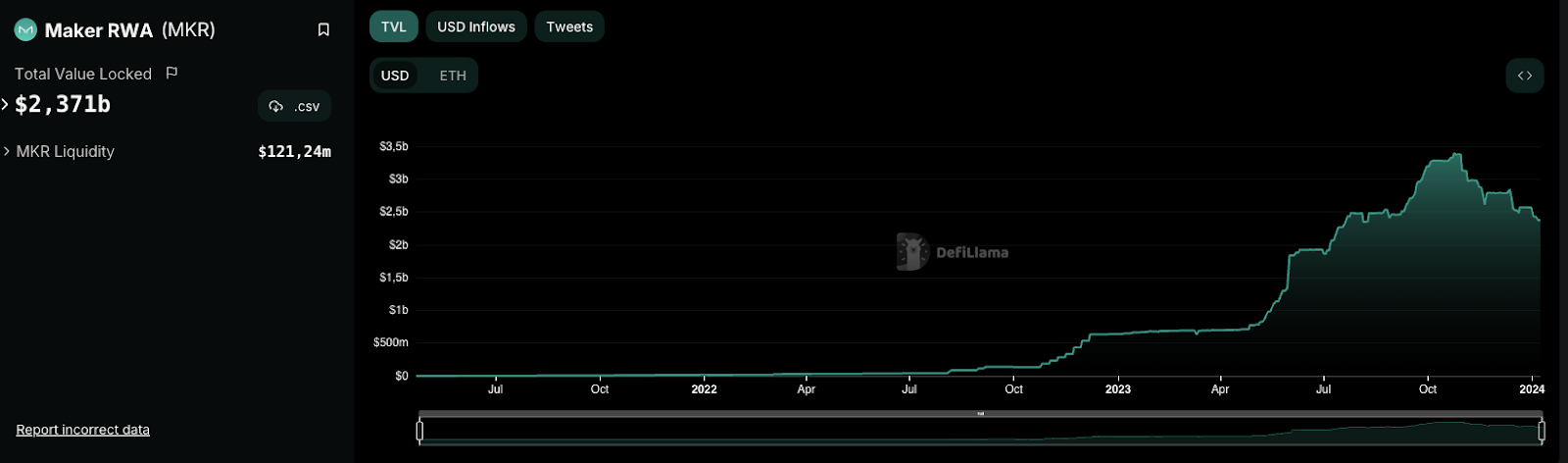

In this specific sector, we find the most capitalized and important dApp in the world of RWAs, namely Maker DAO, the project behind the DAI stablecoin.

DAI is a stablecoin pegged to the dollar and as collateral for its value, in addition to some crypto like WBTC and ETH, there are also short-term U.S. treasuries.

This mechanism has proved very fruitful for Maker, which has managed to bring on-chain returns derived from the world of traditional finance. Today, Maker's RWA department has reached a capitalization of $2.3B, but it has peaked at over $3B.

A similar mechanism is also used by the second most capitalized dApp in this sector, namely stUSDT, where, here too, American bonds are used as a base to offer yield to holders of this stablecoin.

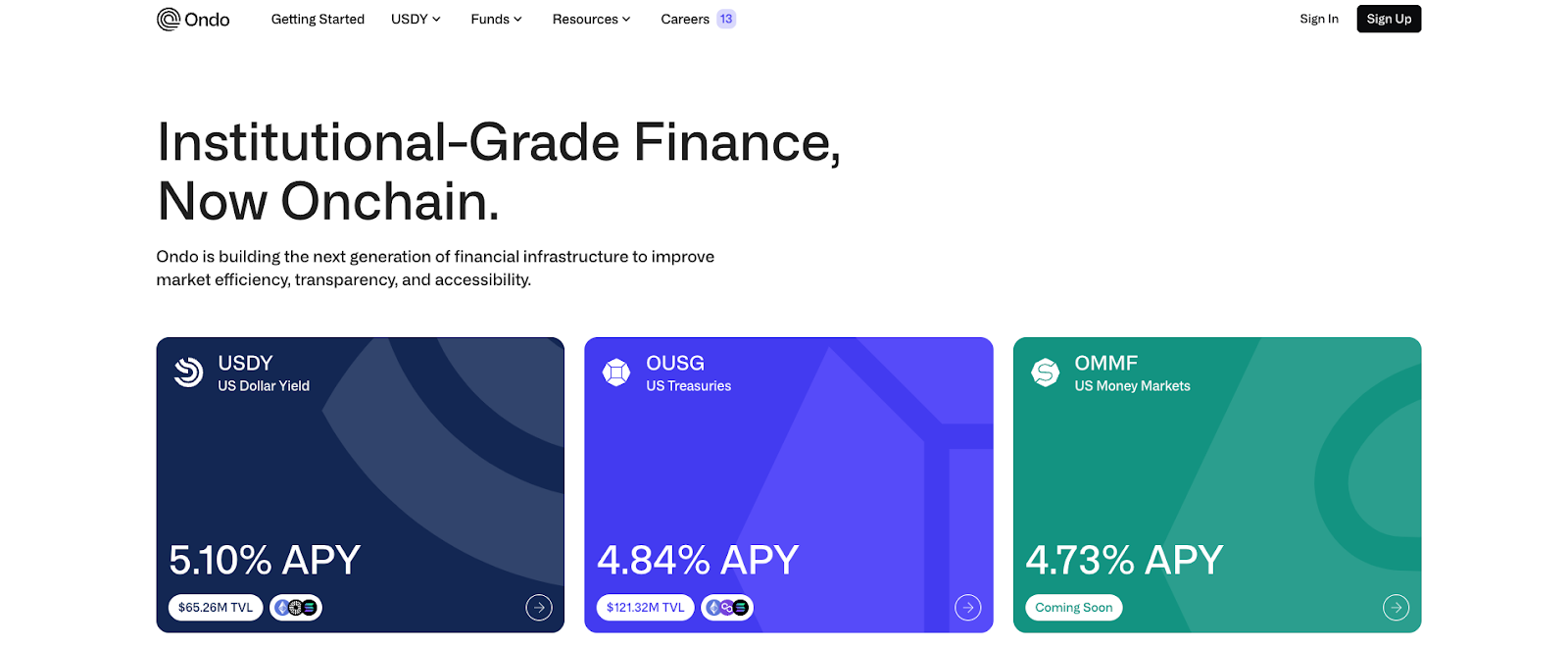

In third place, we find Ondo Finance, a dApp that capitalizes $186 million and aims to give investors the opportunity to expose themselves to markets outside the native crypto ones. Here too, the use of American bonds is the major tokenized asset, so we can already define this as the most used and requested category of RWA today in DeFi.

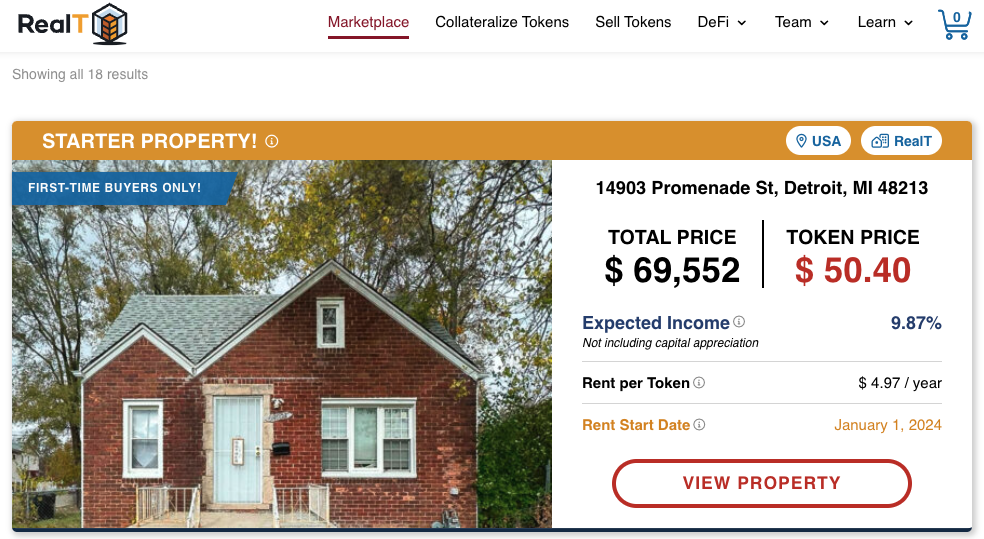

Scrolling down the list, we then find RealT, a dApp that focuses on the real estate market and allows users to buy and sell properties, brought on-chain through a tokenization process. This is the second most developed sector in the RWA ecosystem, with others dApp that use real estate tokenization for bringing different services to the user on-chain.

Synthetix is the leader dApp in the field of the creation of synthetic assets in the world of DeFi. As we said in the introduction of this article, the creation of RWA token could be made in two ways and one of these is by a synthetix process. For the moment Synthetix still has been focused on the creation of synthetix version of on-chain asset, but his structure is already prepared for the creation off-chain asset like commodities or currencies.

The Future of This Sector

After the strong growth seen during this bear market, thanks especially to the use of U.S. treasuries as a yield generator system for DeFi, the sector now seems to be in a standstill where only the most valid projects will continue to exist.

As we have seen in the course of this analysis, the major dApps within this sector are all linked to the concept of on-chain bonds, given the very interesting use case that had been created in recent months.

The evolution of the tokenization of commodities and stocks has experienced slower development than anticipated. Analyzing this situation and its developments will be important for the evolution and implementation of new assets in MetalSwap's Hedging Contracts.

Synthetix currently seems to be one of the most plausible solutions for the creation of these assets, even though they have so far focused on creating native on-chain assets.

Conclusions

DeFi and MetalSwap need other RWAs on-chain besides American bonds, and this will probably be the next big step for the growth of this sector and the entire DeFi.

If decentralized finance wants to continue growing, it will be necessary to bring external assets into this sector, so it's probably just a matter of time before it happens.

That's all for today's episode, but the series on RWAs does not end here. In the next episode, we will specifically analyze the relationship between MetalSwap and RWAs, trying to find solutions to the problem identified earlier.

-The DeFi Foundation

✎ What is MetalSwap?

MetalSwap is a decentralized platform that brings Hedging Contracts on financial markets with the aim of providing coverage to those who work with Digital Assets and an investment opportunity for those who contribute to increase the shared liquidity of the project. Allowing the protection for an increasing number of operators.

With MetalSwap we enable Hedging Contracts on the DeFi field, AMM style.